Quick Read

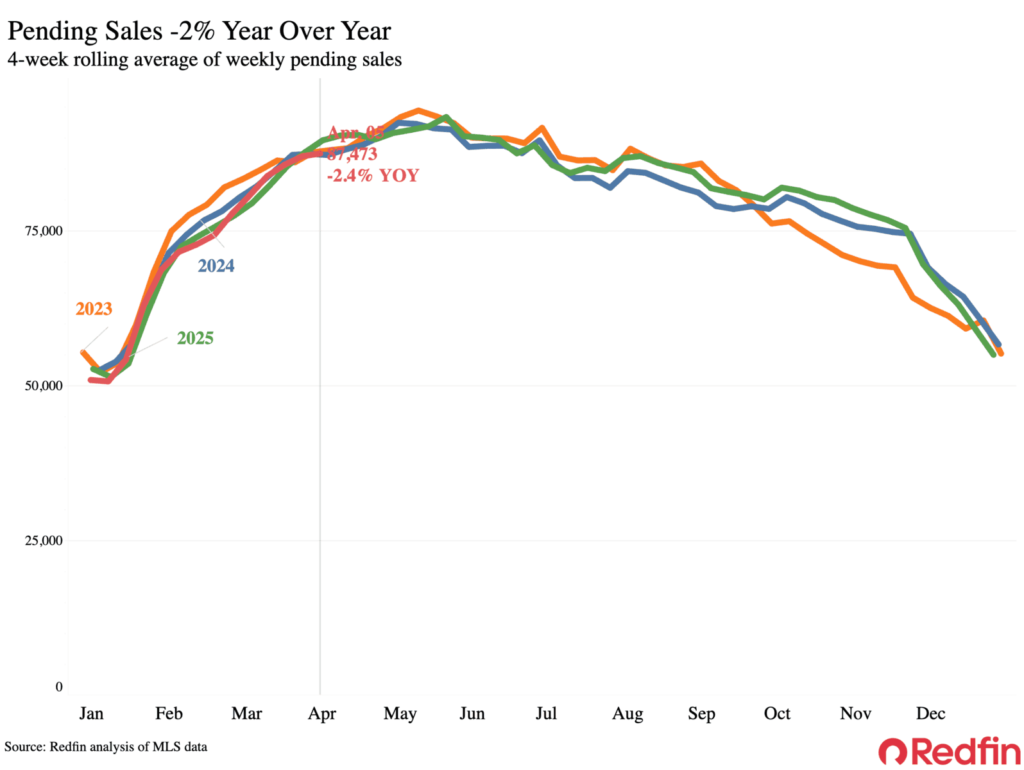

- Pending home sales fell 2.4 percent year-over-year in the four weeks ending April 5, marking the steepest decline in three months, driven largely by mortgage rate spikes linked to the Iran war, per Redfin.

- The weekly average 30-year fixed mortgage rate rose to 6.46 percent by April 2, up from 5.99 percent five weeks prior; economic uncertainty from the conflict is deterring spring homebuyers.

- A ceasefire announcement caused oil prices to drop and markets to rally, potentially easing mortgage rates back into the low-6 percent range, according to economists.

- Despite a 2.2 percent annual rise in home prices and slower sales pace, buyer conditions remain favorable with elevated listings and a median 51-day contract timeline; sellers must focus on strong marketing and home presentation.

An AI tool created this summary, which was based on the text of the article and checked by an editor.

The Iran war sent mortgage rates surging and homebuyers retreating in the four weeks ending April 5, with pending home sales falling 2.4 percent year over year — the biggest decline in three months.

The Iran war sent mortgage rates surging and homebuyers retreating in the four weeks ending April 5, with pending home sales falling 2.4 percent year over year — the steepest drop in three months, according to a new Redfin report.

The weekly average 30-year fixed mortgage rate climbed to 6.46 percent for the week ending April 2, a level not seen since September, up from a four-year low of 5.99 percent just five weeks earlier. As of April 8, the daily average stood at 6.38 percent.

The war is the primary driver of that spike. Market turmoil stemming from the conflict has pushed rates higher and created broad economic unease, sidelining buyers who might otherwise be active this spring.

A ceasefire announced Tuesday offers a potential turning point. Oil prices fell, and markets rallied on the news, and economists say the development could pull mortgage rates back into the low-6 percent range.

The rate environment isn’t the only headwind. Home-sale prices rose 2.2 percent annually, the sharpest annual gain in a year, pushing the median monthly mortgage payment to $2,750. Easter weekend, which fell within this reporting period but not within last year’s comparable window, also temporarily pulled some buyers and sellers off the market. New listings dipped 2.6 percent year over year, the largest decline in a month.

Despite the pullback, conditions still favor buyers in most of the country. Homes that went under contract did so in a median of 51 days nationwide — the slowest pace for this point in the year since 2019 — and active listings remain elevated.

“There are more homes on the market than there are buyers, so sellers need to make sure their house stands out,” said Jesse Landin, a Redfin Premier agent in San Antonio. “The most important day is picture day — that determines whether house hunters will actually walk through your home.”

Landin advised sellers to paint walls, make repairs and hire an agent with a specific marketing plan for their property. “Buyers making large down payments and taking on high monthly payments want a home that’s as close to perfect as possible, because they have more choices in the market,” he said.

Email Jessi Healey